ECONOMICS, BUSINESS AND THE LAW – CONSEQUENCES AND IMPACTS

Many economists and tax experts, among many other specialists, have expressed their opinions on the Tax Reform approved by the National Congress. All of them say, using comparative methods, that the reform is beneficial and more appropriate because it simplifies and modernizes the tax system in force until now.

However, Constitutional Amendment (EC) 132/23, which amends the National Tax System, brought in the principle rules of Tax Law, which are listed below:

- Principles of the Tax System: simplicity, transparency, tax justice, neutrality, cooperation and environmental protection – Article 145, paragraph 3.

- Provision that the Tax on Goods and Services (IBS) and the Contribution on Goods and Services (CBS) will be informed by the principle of neutrality – Article 156-A, paragraph 1.

- Mandate for changes in tax legislation to seek to mitigate regressive effects – Article 145, paragraph 4.

- Bans on the power to tax and limitations:

- expansion of the immunity of temples of any worship, now covering religious entities and including religious welfare and charitable organizations;

- prohibition of taxes on property, income and postal services;

- adequate tax treatment for the cooperative act;

- definition of differentiated and favored treatment for micro-enterprises and small businesses, including special or simplified regimes.

Referring to the III International Tax Law Congress of the IAT, Gustavo Brigagão, in an article, reproduces the various critical points debated by those present on tax reform:

This unjustified haste led to what we have seen: the approval of a constitutional amendment (EC 132/23) marked by mistakes, with the creation of:

- unstructured and topographically confusing standards, with rules on the same subject (special regimes, for example) being regulated either in the constitutional text (specific taxation regimes), or under EC 132/23 (differentiated regimes), or in both texts (favored regimes);

- technically mistaken rules, such as the one that makes non-cumulative credits conditional on payment of the tax by the previous link in the chain; and

- unusual standards, such as the one introduced into the text of PEC 45/19 during its vote in the Chamber of Deputies, granting competence to the states to tax primary and semi-processed products, including beans, which are part of the basic food basket, by means of an odd contribution…

In addition to these arguments, we are going to pragmatically analyze the points, with their counterpoints, the impacts of the reform presented and approved, without any pretension of exhausting them in their entirety.

The starting point is the premise of the reform presented by the government and approved by the National Congress.

Tax reform will bring benefits to the country, to companies and, most importantly, to all Brazilians

Once the Executive presented the set of regulations (bill PLP 68/24), the federal, state and municipal rates were set

The Ministry of Treasury estimates that the reference rate for the new tax system will be 26.5%, of which 8.8% will be CBS (federal) and 17.7% will be IBS (the responsibility of the states and municipalities).

This will be the standard reference rate, applied to goods and services that do not benefit from any kind of differentiated treatment.

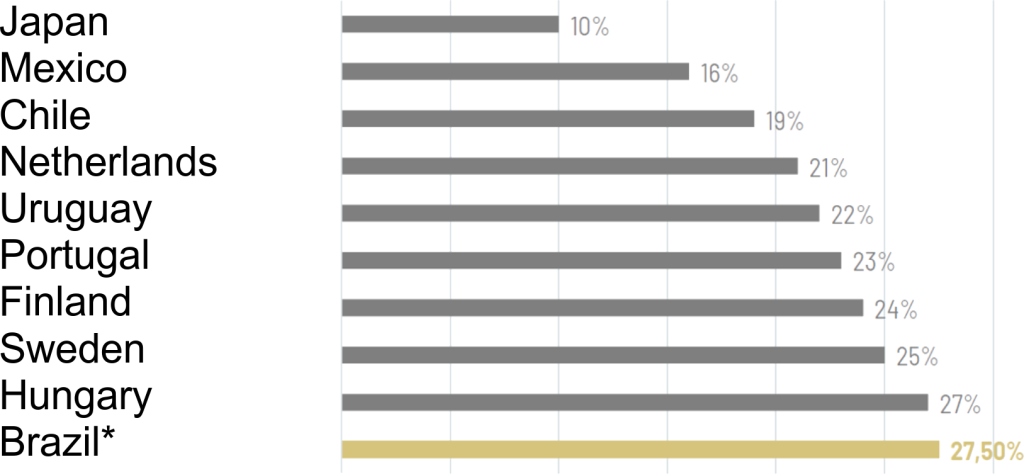

Possibility of reaching the highest VAT rate in the world

*Estimate from the Minister of Treasury, Fernando Haddad, based on the PwC consulting

Source: Agência Senado*

1 – First counterpoint:

The graph above shows that we may have the highest dual Value Added Tax (VAT) rate compared to other countries with a similar tax system.

And why will this happen?

It’s a simple question to answer, but one that economists, specialists and tax experts fail to assess. The tax rates are being set in order to maintain the level of revenue collected by the federal entities in the Brazilian economy at the current level of approximately 34% of GDP.

So much so that any losses in revenue will be managed by the Management Committee, an offsetting fund to be managed by the federal government.

When these limits are set, we see a total distortion of the VAT legal system. Firstly, because dual VAT does not exist in the countries used by the government’s economic team. Secondly, the principles governing VAT – those of neutrality and horizontal equity (comments below) – do not set rates to meet the level of expenditure of the states, not least because a whole is considered and not several states, as in Brazil, in respect of Brazilian Federalism.

For a better understanding of this counterpoint, here is a table of the tax burden over the last three years:

| Tax | 2021 | 2022 | 2023 |

| Total Tax Revenue | 32.64% | 33.07% | 32.44% |

| Federal Government Taxes | 19.87% | 20.59% | 20.09% |

| Tax Budget | 8.74% | 9.43% | 9.11% |

| Social Security Budget | 10.72% | 10.75% | 10.57% |

| Social Security Contribution | 5.00% | 5.15% | 5.27% |

| Cofins (Contribution for the Financing of Social Security) (1) | 2.99% | 2.70% | 2.64% |

| Social Contribution on Net Profit | 1.25% | 1.55% | 1.34% |

| Contribution to PIS/Pasep | 0.83% | 0.78% | 0.76% |

| Government Employees’ Social Security Contribution – CPSS | 0.57% | 0.50% | 0.47% |

| CPMF/IPMF | nd | nd | nd |

| Others | 0.08% | 0.08% | 0.09% |

| Others | 0.41% | 0.41% | 0.42% |

| Education Salary (2) | 0.26% | 0.27% | 0.28% |

| Contr. for Intervention in the Economic Domain (Cide) – Fuels | 0.02% | 0.02% | 0.01% |

| Other Economic and Social Contributions (3) | 0.12% | 0.12% | 0.13% |

| Taxes with a parafiscal destination | 1.78% | 1.82% | 1.90% |

| Contributions to the S System | 0.26% | 0.27% | 0.28% |

| Contribution to FGTS | 1.52% | 1.55% | 1.62% |

| State Government Taxes | 8.81% | 8.48% | 8.12% |

| ICMS | 7.30% | 6.90% | 6.45% |

| IPVA | 0.57% | 0.63% | 0.73% |

| ITCD | 0.14% | 0.13% | 0.14% |

| Contribution to the State Pension System | 0.50% | 0.51% | 0.47% |

| Other State Taxes | 0.30% | 0.32% | 0.32% |

| Municipal Government Taxes | 2.17% | 2.18% | 2.32% |

| ISS | 0.96% | 1.01% | 1.11% |

| IPTU | 0.61% | 0.59% | 0.60% |

| ITBI | 0.22% | 0.19% | 0.19% |

| Contribution to the Municipal Pension System | 0.20% | 0.21% | 0.23% |

| Other Municipal Taxes | 0.19% | 0.19% | 0.19% |

| Memo: GDP | 9.012.142.00 | 10.079.676.68 | 10.856.112.28 |

Source: RFB/MF, for 2021 STN.

2 – Second counterpoint:

The tax base is broad, covering all transactions involving tangible and intangible goods, carried out by legal entities and individuals. In other words, all manufacturers of goods and service providers of any kind – whether legal entities or individuals, such as plumbers, electricians, cleaners, for example (will be the taxpayers of the new taxes).

In the Explanatory Memorandum (EM) No. 00038/2024 MF, it has been established:

Article 1 establishes the IBS and CBS, VAT-type taxes (Value Added Tax), adopted in more than 170 countries, whose main characteristics are: (i) a broad tax base, covering all transactions involving tangible and intangible goods, including rights, and services; (ii)crediting the tax paid on purchases made in the middle of the chain, so that the economic burden falls on the final consumer; and (iii) in more modern models, a limited number of reduced rates and differentiated regimes.

3 – Third counterpoint: THE ECONOMIC BURDEN IS ON THE END CONSUMER,

in other words, whatever the tax regime applicable in the chain of production, trade or provision of services, with any goods (material or immaterial), the economic burden is on the final consumer.

4 – Fourth counterpoint:

Both IBS and CBS are subject to the NEUTRALITY PRINCIPLE, reinforcing the third counterpoint about who will bear the burden of the two taxes.

In addition to this economic aspect, this principle, despite its constitutional provision, has never been adopted in Brazilian legislation, and there are no administrative or judicial precedents on its contours, despite its relevant and economic impact.

Article 2, in line with international VAT models, establishes that the IBS and CBS must be informed by the principle of neutrality, according to which these taxes must avoid distorting consumption decisions and the organization of economic activity. Based on this guideline, the application of the neutrality principle can unfold in several ways.

Thus, all in all, on the basis of the Broad Base and the right to tax credit throughout the production and trade chain, right up to the end consumer, we have that the consumer will pay VAT embedded in the price of goods and services, as follows:

With the price of the product at the producer or merchant = R$ 100.00, the price to the consumer will be R$ 126.50

5 – Fifth counterpoint:

It maintains the adoption of the Non-Cumulative Principle, but with the application of new rules linked to the taxable events, creating the figure of the so-called TAX CREDIT, which corresponds to a refund of taxes paid in the production chain, under conditions, i.e. only for certain operations and only for credits paid on certain operations and not on all operations involving the acquisition of goods and services.

As a general rule, the IBS and CBS levied on the transaction to the final consumer should correspond to the amounts collected throughout the production and marketing chain, so that the economic burden falls on the final consumer. According to VAT models, IBS and CBS are multi-phase taxes, levied on all transactions with goods and services carried out along the chain, up to the final consumer. In conjunction with the incidence rule, and so that there is no cascading taxation (tax on tax), the crediting rule applies: taxpayers in the middle of the chain are entitled to a credit corresponding to the taxes collected on their purchases, so that they only pay the tax authorities the difference between the tax levied on their own operations and the tax collected on their purchases of goods and services. Crediting refers to taxes that have actually been paid and economically corresponds to returning these taxes to the supplier in the form of credits.

The effect of applying the levy and credit rules means that the supplier in the middle of the chain is not burdened by taxes. On the one hand, the IBS and CBS levied on its own operations have been charged to and collected from its purchasers. On the other hand, the IBS and CBS paid on purchases of goods and services by the supplier are fully refunded through crediting. By relieving taxpayers in the middle of the chain, crediting avoids distortions in the organization of economic agents, since the tax burden on the end consumer will be the same regardless of how the production chain is organized5.

6 – Sixth counterpoint:

Regardless of the system adopted to define the taxable event, calculation base or rate, THE TAX BURDEN ON THE END CONSUMER WILL BE THE SAME.

International experience and the guidelines of the Organization for Economic Cooperation and Development (OECD) point to other developments in the principle of neutrality. Taxpayers in similar situations who carry out similar operations should be subject to similar VAT taxation. This means that VAT must be isonomic in similar circumstances, which is known in the literature as horizontal equity6.

7 – Seventh counterpoint:

The new taxes will be governed by a new principle: HORIZONTAL EQUITY, considered to be a consequence of the Principle of Neutrality – taxpayers in similar situations carrying out similar operations should be subject to the same taxation (isonomic character in similar circumstances). It seems to be a new version of the Principle of Contributory Capacity and/or Tax Equality, or Tax Isonomy. But the question remains: if the economic burden of the new taxes falls on the end consumer, what is the real purpose of this new principle in the production and distribution chain?

8 – Eighth counterpoint:

If the new system is valid for operations carried out in national territory, and this is what was approved by the Constitutional Amendment, what is the purpose of including the Principle of Neutrality to ensure equivalent tax treatment for resident and non-resident taxpayers?

In addition, neutrality can also be applied in international trade, by ensuring equivalent tax treatment for resident and non-resident taxpayers7.

9 – Ninth counterpoint:

The Constitutional Amendment brings another new principle into the tax system – that of anti-abuse rules. Will it replace the rules and precedents that deal with tax evasion and avoidance? Or is it a new rule to put an end to Tax Planning? What are these new anti-abuse rules?

10 – Tenth counterpoint:

When dealing with the calculation basis, EC 132/23 includes various third-party operations and values that are subject to IBS and CBS, showing the unconstitutional double incidence.

We hope that the National Congress, through the Senate and the House of Representatives, will review all these points, so that we can effectively have a new tax regime that simplifies the system and is effectively beneficial to society as a whole, so that, in transactions involving goods and services, by passing on the entire economic and financial burden to the Brazilian consumer, they don’t finance the public deficit and can purchase goods and services without the high tax burden of 26.5%.

So, the question remains:

Will the Tax Reform bring benefits to the country, to companies and, most importantly, to all Brazilians?